Fuelled by an expanding economy and rising wealth, China's gold jewellery demand has boomed since the early 2000s.

China's demand shrank by one-third between 2013 and 2016. But having gone through a period of reinvention, demand is showing signs of renewed growth. Jewellers’ efforts to modernise their product mix, improve design, and seamlessly blend customers’ online and offline experiences are starting to bear fruit. It is our view that China’s jewellery industry has turned a corner. We believe a more consumer-focused industry, combined with China’s rising wealth, will support global gold demand and gold’s long-term performance.

Industry revival

China's gold jewellery demand more than tripled over the past 15 years as the economy expanded and individual wealth grew. It is now the largest gold jewellery market in the world, accounting for 30% of global demand.1 But it hasn’t all been plain sailing. The 2013 boom – when tumbling gold prices sparked a buying frenzy – saddled the sector with a record number of stores, excess capacity, and fierce price wars. The industry was forced to go through a painful period of reinvention. Rather than relying on traditional consumers wanting to buy gold jewellery purely for its gold content, jewellers made efforts to get to know their customers better. Now, they increasingly try to meet the needs of modern consumers by offering a more diverse product mix, designing more appealing jewellery and optimising sales channels.

Changing consumers

Whilst China’s economy is famously regarded as multi-tier, increasingly it is driven by middle-class and affluent consumers who desire luxury goods, and this includes gold jewellery.

But China’s middle-class is evolving and, over recent years, the profile of China’s jewellery consumers has changed. In 2016 we conducted a detailed piece of consumer research in which we questioned 2,000 women; 2 this highlighted two interesting trends:

• Consumer preferences differ by region

• Tastes differ across age groups.

Consumer preferences by region

In recent years, gold jewellery has faced stiff competition from other items of jewellery and luxury goods in Tier 1 (T1) cities.3 According to our consumer research, 18% of women in T1 cities would choose to buy gold jewellery when given RMB 5,000, compared with 14% and 15% who would buy diamond or platinum jewellery respectively (Figure 1). The competition is not as fierce in lower tier cities: consumers in T3 and T4 flock to buy high carat, heavy gold jewellery for wealth preservation purposes. As Figure 1 shows, 24% of women surveyed in T3 and T4 cities would choose gold, compared with 8% choosing platinum and 12% choosing diamond jewellery.

Tastes across age groups

Gold jewellery faces particular pressure among millennial consumers, who desire social acceptance yet wish to demonstrate their individuality. Gold jewellery finds itself increasingly in competition with technology (smartphone/wearables) and fashion. When asked what they would buy if they were given RMB 5,000, only 9% of those between 18-25 years opted for gold jewellery, compared with 31% who chose technology, such as smartphones or wearable technology (Figure 2). Gold found greater favour among older consumers. For women in the 26+ year category, 24% opted for gold, compared with 23% for designer fashion and 20% for technology. These issues matter because T1 cities and millennials are changing the shape of consumerism in China. Trends that start amongst these groups eventually filter through the consumer landscape.

While this has challenged the gold jewellers, it also represents an opportunity. Consumers in T1 cities contribute around 40% of total national spending, while the growth rate of spending by people born after 1990 is twice that of those born between 1970 and 1979.4 And consumers born post-1990 perform over half of their spending online. By comparison, the proportion was only one-third for those born between 1970 and 1989. Successfully engaging with these consumers is key to the future health of China’s gold jewellery market. Jewellers’ strategy reboot China’s jewellery industry has responded to the changing consumer landscape over recent years. It has adopted two main strategies: offering an improved product range and blending the online and offline retail experience.

Improving product offering

24ct gold jewellery has dominated China’s gold jewellery market. It resonates well with older, more traditional consumers. But young, city folk have different tastes. 18ct gold (also known as K-gold) has played an important role in meeting the needs of this part of the market for some time. And more recently, the jewellery industry has developed 22ct gold. Both 18ct and 22ct gold jewellery are viewed as more fashionable and affordable in comparison to traditional 24ct gold. 18ct red gold – the colour obtained from a gold copper alloy – is more popular with young women who tend to buy it as a reward or a treat, perhaps partly because of its romantic name of “rose gold”.

As well as meeting consumers’ desires, these products offer fatter profits for retailers. 24ct jewellery is usually sold by weight, with slim margins. K-gold is sold by piece, which allows the retailer to boost profit margins. Jewellers have also uncovered ways to offer intricately designed pieces that meet lower budgets. 3D hard gold enables this shift to thrift. A special chemical process makes 3D gold four times harder than 24ct gold. Yet it uses only one-third of the gold that traditional jewellery uses to produce a same-sized piece, making it much more affordable. Jewellery retailer Chow Tai Fook was an early adopter of these developments. Its 3D Fuxing Baobao (‘Lucky Mascot Babies’) series was well received by consumers and has generated good sales revenue, according to the jeweller. In addition, more and more jewellers are using renowned intellectual property to leap into the millennials’ mind. Chow Tai Fook’s Disney Tsum Tsum collection is an example of the successful marriage between much-loved characters and stunning jewellery design, and is sought after by fans of all ages.

Blending the online/offline experience

The jewellery industry has improved the interplay between customers’ online and offline experiences. Our consumer research shows that although around one-third of gold purchasers begin their journey online, only 4% go on to complete their purchase online.6 A desire to touch the product and concerns around the security of online purchases are the principle reasons cited for preferring to buy in-store. Other value-added services such as free cleaning, maintenance and buy-back schemes suggest online jewellery shops cannot fully replace the trip to a bricks-andmortar shop. And in the short- to medium-term, online shops are unlikely to take more than a small share of the market. Nevertheless, online shops are an important part of retailers’ marketing plans. Smart jewellers have leveraged the many online shopping festivals, such as the Double 11 Single's Day,7 to drive sales offline. Anecdotally, one prominent jeweller noted that such online sales events boosted its in-store sales five-fold. Greater effort is being made to cater to the behaviours of online shoppers. Because many are young, jewellers focus their online offerings on lighter-weight pieces and K-gold jewellery, usually priced below RMB 2,000 (US$300). What’s more, the trail of clicks left by online shoppers helps jewellers to understand modern customers better, faster and with lower communication costs. A jeweller can easily see which items sell the most and target advertisements more efficiently using data collected responsibly across its all-inclusive ecosystem. For example, clicks on banner advertisements, products, items saved in ‘wish lists’ and those purchases at check-out can provide actionable insight to improve the performance of both digital and physical stores.

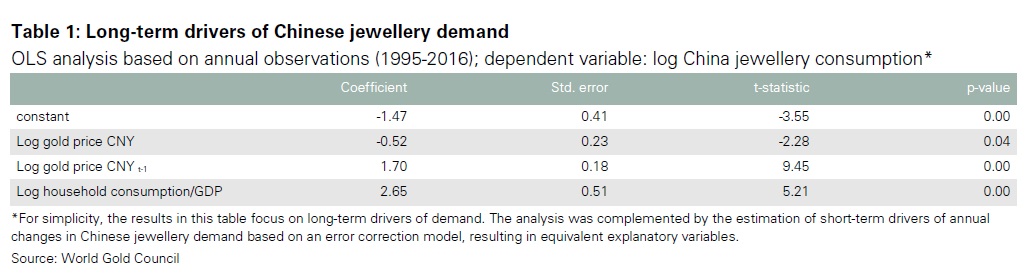

Long-term drivers of jewellery demand Many cultural and historical factors underpin the significance of gold for consumers around the world. A quantitative analysis of the data, however, reveals that consumer demand is driven by two very intuitive factors: price and income. Our analysis, based on an error-correction model aimed at capturing short- and long-run drivers, shows that this is true for Chinese jewellery demand. The analysis, using data from 1995 to 2016, shows that gold demand is explained by (i) the current local price of gold, (ii) the local gold price the previous year, and (iii) consumers’ income (Table 1):

• Consistent with economic theory, current demand is negatively associated with current prices. Higher prices imply less demand and vice versa.

• However, current demand is also positively related to prices in the previous year. This suggests that jewellery demand is also influenced by the price trend of gold: if the gold price shows an upward trend, consumers are more likely to buy gold (despite higher prices) because they see a long-term benefit, while a downward trend may deter future consumers.

• Demand rises more than 1-for-1 with income growth – in economics this is a characteristic of ‘superior goods’.

We found that the proxy for consumers’ income that produced the best results was household expenditure relative to GDP. When household spending is relatively high compared to GDP, consumers are confident and feel wealthier, and this promotes the ‘superior good’ effect. This proxy also captures the growing importance of the consumer in China. All else being equal, China’s shift towards a consumer-driven economy should bode well for jewellery demand over the coming years.

Further opportunities

China’s jewellers have made encouraging progress in recent years. But more can be done. Through our field research we have identified three areas on which the industry can focus in order to drive sales.

Build brands that emotionally connect with consumers

China’s gold jewellery retail landscape is dominated by onesize- fits-all megastores, with little differentiation between brands. This may work when targeting the traditional gold jewellery buyer who is focused purely on jewellery’s gold content, but may not be the most effective way to satisfy the needs of young millennials who want jewellery that reflects their unique style and marks their success. Strong brands have the capacity to build an emotional connection between these aspirations and gold. Success stories, such as that of Danish jeweller Pandora, highlight how branding can instil customer loyalty and boost margins.9 It can help jewellers to win new customers while retaining old ones and can provide a launch pad for new products. Jewellers in China have started to launch product series targeted to specific customer segments. But, in the main, these are branded no differently. The creation of subbrands could be an effective way of reaching and building loyalty among a new target audience. Chow Tai Fook is a good example of a retailer that has adopted this strategy. It launched Monologue and Soinlove brands aimed at the young consumer. Instead of selling these new products in its main store, it invested in new boutique-style stores, fully branded with the two new identities. Its success exemplifies how well this brave strategy can work and provides an interesting case study for other retailers. In addition, jewellers should also be aware that their image is shaped by customer experience as much as by advertising and marketing. Beijing Caibai, for example, positions itself as the provider of “a one-stop service for all things gold jewellery”. It devotes a large shopping area to polish and repair items of jewellery and routinely organises seminars in local neighbourhoods.

Ensure brands are trusted

Trust and transparency are the currencies of consumer loyalty. Trust can cement customer relationships but to build trust, jewellers should consider two areas. The first is to ensure they are transparent in their customer dealings and that consumers understand exactly what they are buying. Some retailers have started selling lower carat gold jewellery plated with 24ct gold without clearly communicating exact product specifications. Consumers can find this confusing. China’s jewellery industry should also pay attention to environmental and social issues. Such issues are becoming increasingly important for consumers, and are clearly of government interest too. Gold jewellers need to be alert to this sentiment. For example, the treatment of ultra-high purity (99.999%) gold jewellery requires a special chemical process that is pollutive. Rather than build a brand focused on the high purity of gold, jewellers could focus on responsibly sourcing and producing gold jewellery to meet the ethical desires of consumers. In our survey, 46% of respondents said it was either extremely important or very important for the jewellery and luxury fashion items they buy to be produced ethically. By contrast, only 28% agreed that it was extremely important or very important for the jewellery or luxury item to be associated with tradition, yet this is where the key focus of the jewellery industry lies at present.

Create more buying occasions

24ct gold jewellery is bought infrequently – buying occasions are focused around the Lunar New Year, weddings and births. The introduction of K-gold and 3D hard gold has attracted younger customers, but these products could also be used to increase shopping frequency among more traditional customers. Better use of online platforms and social media will help. Millennials are the “everything new and everything now” generation, so a convenient shopping button to place orders can immediately turn interest into action. Online buyers should be granted the same benefits as offline customers. Currently, these two groups are, more often than not, treated as independent and insulated from each other. This creates additional communication costs and misses opportunities to glean valuable data. For example, we know that birthdays are now the biggest occasion for gold jewellery and other luxury fashion purchases. If data around these purchases were collected responsibly from both online and offline buyers, an automatic promotional push message could be sent to the buyer each year before their birthday or other anniversaries.

Summary

China’s jewellery market is emerging from a tough few years, having developed better strategies to engage with modern consumers. While good progress has been made, we believe the industry can do more. Developing brands and creating new buying occasions will help jewellers meet the needs of China’s modern consumers. This, combined with China’s increasingly consumer-driven economy, should support the Chinese and global gold market.

Be the first to comment