Post By : IJ News ServiceOn 15 October 2014 12:52 AM

{{Rio Tinto}} is confident that the medium to long-term fundamentals for the diamond industry are positive with an anticipated material supply shortfall which will drive price growth. Rough diamond prices are expected to improve further.%%

{{Share in World Production :}}%%

This mining giant accounts for about six per cent of the world production of rough diamonds by value. However, diamonds accounts for a small portion of its overall business which comprises aluminium, copper, coal, iron ore, uranium, gold and some industrial materials (like borates, titanium dioxide, salt, talc and zircon) apart from rough diamonds.%%

{{Independent Marketing :}}%%

Rio Tinto has been in diamond business for nearly 25 years by now and has been marketing its rough diamonds independently since 1996. It aspires to be the preferred supplier of rough diamonds.%%

{{Operating 3 Mines :}}%%

It operates three diamond mines at different locations. It owns 100 per cent the Argyle mine in Australia and has 60 per cent stake in the Diavik (Canada) and 77.8 per cent interest in Murowa (Zimbabwe).%%

{{Impact of Economic Turmoil :}}%%

According to Rio Tinto, the unprecedented turmoil last year severely affected demand for rough diamonds which was highly reliant on the US economy. Rio Tinto acted quickly to minimize operating and capital costs and slow-down its underground mining projects at both Argyle and Diavik mines. It also took steps to curtail production.

{{Argyle :}}%%

Argyle has been known as the world’s largest producer of rough diamonds by volume. Also, it produces some rare pink diamonds which are highly valued. These are being sold in the form of loose polished pinks.$$

The Argyle mine is being operated as an open-pit mine at present. Such operations are expected to continue till 2012. There after the operations there will go underground. It is expected that the underground mining will continue there until at least 2018.%%

{{Underground Projects :}}%%

During 2009, construction of the underground project was slowed by reducing the project workforce and delaying completion of development. First production from the underground operation is now expected in 2012.%%

{{Diavik :}}%%

Production from Diavik’s open pit operations is expected to continue through to 2012. Thereafter, the mine will turn fully to underground operations.$$

In 2009, operations at Diavik were suspended for six weeks in view of the deterioration in global market conditions. This, together with the lower grade feed ore, reduced diamond production (Rio Tinto share) to 3.3 million carats from 5.5 million carats in the earlier year.

Open pit mining at A 154 neared completion in 2009, with activity transitioning to the lower grade A-418 pipe.%%

{{Murowa :}}%%

The Murowa mine has been operating since 2004 as a small open-pit mine. Rio Tinto group’s share in its production in 2009 declined to 97000 carats, from 2,05,000 carats in 2008 as a result of lower ore grade and the delayed project to deal with the changing ore characteristics.$$

Morawa is considering expanding the existing open-pit to increase production. The previous feasibility study for this expansion is currently being reviewed and discussions are being held with the Zimbabwe Government on the investment environment that is required to support this project.

{{Bunder Project :}}%%

The Rio Tinto group is actively pursuing the Bunder Diamond Project in India which looks promising. During 2009, a 10-tonne per hour bulk-sampling treatment plant was commissioned there. It has already commenced the processing of bulk samples for further evaluation work.%%

{{Market Condition : }}%%

After a sharp set-back in the market for rough diamonds in the first quarter of 2009, prices started recovering from the second half of the year. Rio Tinto’s diamond division is of the view that the market will continue to be dependent in the recovery of US consumer sentiment though the robust growth of jewellery consumption in the smaller but important Chinese and Indian markets will provide some underlying support to both prices and volumes.%%

{{Impact of Financial Crisis :}}%%

The financial crisis that started in the latter half of 2008 and was quite acute in the earlier part of 2009 had a severe impact on the global demand for diamonds. Producers of rough diamonds were forced to resort to production cut backs Rio Tinto was also constrained to do so.

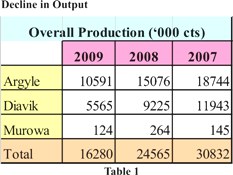

{{Decline in Output :}}%%

Overall production at all the three mines operated by Rio Tinto came down sharply as can be seen from the following production data :(See table 1)

As these figures reveal the total production of diamonds at three locations fell from 30.832 million carats in 2007 to 24.565 million carats in 2008 and dwindled further to 16.280 million carats in 2009, with the overall decline in demand.

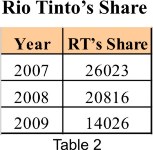

{{Rio Tinto’s Share :}}

Consequently the share of Rio Tinto in the overall production also came down as under (in ‘000 carats), (See table 2)

With the decline in production, sales revenue also went down, as also the net earnings from this business.%%

{{Impact on Revenue, Earnings :}}%%

With the sharp decline in production, revenue as well as net earnings from Rio Tinto’s diamond business came down. The revenue in 2009 was down at US$ 450 million, compared with US$ 840 million in 2008. Diamond business which resulted in net earnings of US$ 137 million in 2008, brought a negative return of US$ 68 million in 2009. Of course, both the demand and prices for diamonds are now showing an improved trend. The diamond business is therefore expected to present much better performance for 2010.

{{Rio Tinto}} is confident that the medium to long-term fundamentals for the diamond industry are positive with an anticipated material supply shortfall which will drive price growth. Rough diamond prices are expected to improve further.%%

{{Share in World Production :}}%%

This mining giant accounts for about six per cent of the world production of rough diamonds by value. However, diamonds accounts for a small portion of its overall business which comprises aluminium, copper, coal, iron ore, uranium, gold and some industrial materials (like borates, titanium dioxide, salt, talc and zircon) apart from rough diamonds.%%

{{Independent Marketing :}}%%

Rio Tinto has been in diamond business for nearly 25 years by now and has been marketing its rough diamonds independently since 1996. It aspires to be the preferred supplier of rough diamonds.%%

{{Operating 3 Mines :}}%%

It operates three diamond mines at different locations. It owns 100 per cent the Argyle mine in Australia and has 60 per cent stake in the Diavik (Canada) and 77.8 per cent interest in Murowa (Zimbabwe).%%

{{Impact of Economic Turmoil :}}%%

According to Rio Tinto, the unprecedented turmoil last year severely affected demand for rough diamonds which was highly reliant on the US economy. Rio Tinto acted quickly to minimize operating and capital costs and slow-down its underground mining projects at both Argyle and Diavik mines. It also took steps to curtail production.

{{Argyle :}}%%

Argyle has been known as the world’s largest producer of rough diamonds by volume. Also, it produces some rare pink diamonds which are highly valued. These are being sold in the form of loose polished pinks.$$

The Argyle mine is being operated as an open-pit mine at present. Such operations are expected to continue till 2012. There after the operations there will go underground. It is expected that the underground mining will continue there until at least 2018.%%

{{Underground Projects :}}%%

During 2009, construction of the underground project was slowed by reducing the project workforce and delaying completion of development. First production from the underground operation is now expected in 2012.%%

{{Diavik :}}%%

Production from Diavik’s open pit operations is expected to continue through to 2012. Thereafter, the mine will turn fully to underground operations.$$

In 2009, operations at Diavik were suspended for six weeks in view of the deterioration in global market conditions. This, together with the lower grade feed ore, reduced diamond production (Rio Tinto share) to 3.3 million carats from 5.5 million carats in the earlier year.

Open pit mining at A 154 neared completion in 2009, with activity transitioning to the lower grade A-418 pipe.%%

{{Murowa :}}%%

The Murowa mine has been operating since 2004 as a small open-pit mine. Rio Tinto group’s share in its production in 2009 declined to 97000 carats, from 2,05,000 carats in 2008 as a result of lower ore grade and the delayed project to deal with the changing ore characteristics.$$

Morawa is considering expanding the existing open-pit to increase production. The previous feasibility study for this expansion is currently being reviewed and discussions are being held with the Zimbabwe Government on the investment environment that is required to support this project.

{{Bunder Project :}}%%

The Rio Tinto group is actively pursuing the Bunder Diamond Project in India which looks promising. During 2009, a 10-tonne per hour bulk-sampling treatment plant was commissioned there. It has already commenced the processing of bulk samples for further evaluation work.%%

{{Market Condition : }}%%

After a sharp set-back in the market for rough diamonds in the first quarter of 2009, prices started recovering from the second half of the year. Rio Tinto’s diamond division is of the view that the market will continue to be dependent in the recovery of US consumer sentiment though the robust growth of jewellery consumption in the smaller but important Chinese and Indian markets will provide some underlying support to both prices and volumes.%%

{{Impact of Financial Crisis :}}%%

The financial crisis that started in the latter half of 2008 and was quite acute in the earlier part of 2009 had a severe impact on the global demand for diamonds. Producers of rough diamonds were forced to resort to production cut backs Rio Tinto was also constrained to do so.

{{Decline in Output :}}%%

Overall production at all the three mines operated by Rio Tinto came down sharply as can be seen from the following production data :(See table 1)

As these figures reveal the total production of diamonds at three locations fell from 30.832 million carats in 2007 to 24.565 million carats in 2008 and dwindled further to 16.280 million carats in 2009, with the overall decline in demand.

{{Rio Tinto’s Share :}}

Consequently the share of Rio Tinto in the overall production also came down as under (in ‘000 carats), (See table 2)

With the decline in production, sales revenue also went down, as also the net earnings from this business.%%

{{Impact on Revenue, Earnings :}}%%

With the sharp decline in production, revenue as well as net earnings from Rio Tinto’s diamond business came down. The revenue in 2009 was down at US$ 450 million, compared with US$ 840 million in 2008. Diamond business which resulted in net earnings of US$ 137 million in 2008, brought a negative return of US$ 68 million in 2009. Of course, both the demand and prices for diamonds are now showing an improved trend. The diamond business is therefore expected to present much better performance for 2010.

{{Rio Tinto}} is confident that the medium to long-term fundamentals for the diamond industry are positive with an anticipated material supply shortfall which will drive price growth. Rough diamond prices are expected to improve further.%%

{{Share in World Production :}}%%

This mining giant accounts for about six per cent of the world production of rough diamonds by value. However, diamonds accounts for a small portion of its overall business which comprises aluminium, copper, coal, iron ore, uranium, gold and some industrial materials (like borates, titanium dioxide, salt, talc and zircon) apart from rough diamonds.%%

{{Independent Marketing :}}%%

Rio Tinto has been in diamond business for nearly 25 years by now and has been marketing its rough diamonds independently since 1996. It aspires to be the preferred supplier of rough diamonds.%%

{{Operating 3 Mines :}}%%

It operates three diamond mines at different locations. It owns 100 per cent the Argyle mine in Australia and has 60 per cent stake in the Diavik (Canada) and 77.8 per cent interest in Murowa (Zimbabwe).%%

{{Impact of Economic Turmoil :}}%%

According to Rio Tinto, the unprecedented turmoil last year severely affected demand for rough diamonds which was highly reliant on the US economy. Rio Tinto acted quickly to minimize operating and capital costs and slow-down its underground mining projects at both Argyle and Diavik mines. It also took steps to curtail production.

{{Argyle :}}%%

Argyle has been known as the world’s largest producer of rough diamonds by volume. Also, it produces some rare pink diamonds which are highly valued. These are being sold in the form of loose polished pinks.$$

The Argyle mine is being operated as an open-pit mine at present. Such operations are expected to continue till 2012. There after the operations there will go underground. It is expected that the underground mining will continue there until at least 2018.%%

{{Underground Projects :}}%%

During 2009, construction of the underground project was slowed by reducing the project workforce and delaying completion of development. First production from the underground operation is now expected in 2012.%%

{{Diavik :}}%%

Production from Diavik’s open pit operations is expected to continue through to 2012. Thereafter, the mine will turn fully to underground operations.$$

In 2009, operations at Diavik were suspended for six weeks in view of the deterioration in global market conditions. This, together with the lower grade feed ore, reduced diamond production (Rio Tinto share) to 3.3 million carats from 5.5 million carats in the earlier year.

Open pit mining at A 154 neared completion in 2009, with activity transitioning to the lower grade A-418 pipe.%%

{{Murowa :}}%%

The Murowa mine has been operating since 2004 as a small open-pit mine. Rio Tinto group’s share in its production in 2009 declined to 97000 carats, from 2,05,000 carats in 2008 as a result of lower ore grade and the delayed project to deal with the changing ore characteristics.$$

Morawa is considering expanding the existing open-pit to increase production. The previous feasibility study for this expansion is currently being reviewed and discussions are being held with the Zimbabwe Government on the investment environment that is required to support this project.

{{Bunder Project :}}%%

The Rio Tinto group is actively pursuing the Bunder Diamond Project in India which looks promising. During 2009, a 10-tonne per hour bulk-sampling treatment plant was commissioned there. It has already commenced the processing of bulk samples for further evaluation work.%%

{{Market Condition : }}%%

After a sharp set-back in the market for rough diamonds in the first quarter of 2009, prices started recovering from the second half of the year. Rio Tinto’s diamond division is of the view that the market will continue to be dependent in the recovery of US consumer sentiment though the robust growth of jewellery consumption in the smaller but important Chinese and Indian markets will provide some underlying support to both prices and volumes.%%

{{Impact of Financial Crisis :}}%%

The financial crisis that started in the latter half of 2008 and was quite acute in the earlier part of 2009 had a severe impact on the global demand for diamonds. Producers of rough diamonds were forced to resort to production cut backs Rio Tinto was also constrained to do so.

{{Decline in Output :}}%%

Overall production at all the three mines operated by Rio Tinto came down sharply as can be seen from the following production data :(See table 1)

As these figures reveal the total production of diamonds at three locations fell from 30.832 million carats in 2007 to 24.565 million carats in 2008 and dwindled further to 16.280 million carats in 2009, with the overall decline in demand.

{{Rio Tinto’s Share :}}

Consequently the share of Rio Tinto in the overall production also came down as under (in ‘000 carats), (See table 2)

With the decline in production, sales revenue also went down, as also the net earnings from this business.%%

{{Impact on Revenue, Earnings :}}%%

With the sharp decline in production, revenue as well as net earnings from Rio Tinto’s diamond business came down. The revenue in 2009 was down at US$ 450 million, compared with US$ 840 million in 2008. Diamond business which resulted in net earnings of US$ 137 million in 2008, brought a negative return of US$ 68 million in 2009. Of course, both the demand and prices for diamonds are now showing an improved trend. The diamond business is therefore expected to present much better performance for 2010.

{{Rio Tinto}} is confident that the medium to long-term fundamentals for the diamond industry are positive with an anticipated material supply shortfall which will drive price growth. Rough diamond prices are expected to improve further.%%

{{Share in World Production :}}%%

This mining giant accounts for about six per cent of the world production of rough diamonds by value. However, diamonds accounts for a small portion of its overall business which comprises aluminium, copper, coal, iron ore, uranium, gold and some industrial materials (like borates, titanium dioxide, salt, talc and zircon) apart from rough diamonds.%%

{{Independent Marketing :}}%%

Rio Tinto has been in diamond business for nearly 25 years by now and has been marketing its rough diamonds independently since 1996. It aspires to be the preferred supplier of rough diamonds.%%

{{Operating 3 Mines :}}%%

It operates three diamond mines at different locations. It owns 100 per cent the Argyle mine in Australia and has 60 per cent stake in the Diavik (Canada) and 77.8 per cent interest in Murowa (Zimbabwe).%%

{{Impact of Economic Turmoil :}}%%

According to Rio Tinto, the unprecedented turmoil last year severely affected demand for rough diamonds which was highly reliant on the US economy. Rio Tinto acted quickly to minimize operating and capital costs and slow-down its underground mining projects at both Argyle and Diavik mines. It also took steps to curtail production.

{{Argyle :}}%%

Argyle has been known as the world’s largest producer of rough diamonds by volume. Also, it produces some rare pink diamonds which are highly valued. These are being sold in the form of loose polished pinks.$$

The Argyle mine is being operated as an open-pit mine at present. Such operations are expected to continue till 2012. There after the operations there will go underground. It is expected that the underground mining will continue there until at least 2018.%%

{{Underground Projects :}}%%

During 2009, construction of the underground project was slowed by reducing the project workforce and delaying completion of development. First production from the underground operation is now expected in 2012.%%

{{Diavik :}}%%

Production from Diavik’s open pit operations is expected to continue through to 2012. Thereafter, the mine will turn fully to underground operations.$$

In 2009, operations at Diavik were suspended for six weeks in view of the deterioration in global market conditions. This, together with the lower grade feed ore, reduced diamond production (Rio Tinto share) to 3.3 million carats from 5.5 million carats in the earlier year.

Open pit mining at A 154 neared completion in 2009, with activity transitioning to the lower grade A-418 pipe.%%

{{Murowa :}}%%

The Murowa mine has been operating since 2004 as a small open-pit mine. Rio Tinto group’s share in its production in 2009 declined to 97000 carats, from 2,05,000 carats in 2008 as a result of lower ore grade and the delayed project to deal with the changing ore characteristics.$$

Morawa is considering expanding the existing open-pit to increase production. The previous feasibility study for this expansion is currently being reviewed and discussions are being held with the Zimbabwe Government on the investment environment that is required to support this project.

{{Bunder Project :}}%%

The Rio Tinto group is actively pursuing the Bunder Diamond Project in India which looks promising. During 2009, a 10-tonne per hour bulk-sampling treatment plant was commissioned there. It has already commenced the processing of bulk samples for further evaluation work.%%

{{Market Condition : }}%%

After a sharp set-back in the market for rough diamonds in the first quarter of 2009, prices started recovering from the second half of the year. Rio Tinto’s diamond division is of the view that the market will continue to be dependent in the recovery of US consumer sentiment though the robust growth of jewellery consumption in the smaller but important Chinese and Indian markets will provide some underlying support to both prices and volumes.%%

{{Impact of Financial Crisis :}}%%

The financial crisis that started in the latter half of 2008 and was quite acute in the earlier part of 2009 had a severe impact on the global demand for diamonds. Producers of rough diamonds were forced to resort to production cut backs Rio Tinto was also constrained to do so.

{{Decline in Output :}}%%

Overall production at all the three mines operated by Rio Tinto came down sharply as can be seen from the following production data :(See table 1)

As these figures reveal the total production of diamonds at three locations fell from 30.832 million carats in 2007 to 24.565 million carats in 2008 and dwindled further to 16.280 million carats in 2009, with the overall decline in demand.

{{Rio Tinto’s Share :}}

Consequently the share of Rio Tinto in the overall production also came down as under (in ‘000 carats), (See table 2)

With the decline in production, sales revenue also went down, as also the net earnings from this business.%%

{{Impact on Revenue, Earnings :}}%%

With the sharp decline in production, revenue as well as net earnings from Rio Tinto’s diamond business came down. The revenue in 2009 was down at US$ 450 million, compared with US$ 840 million in 2008. Diamond business which resulted in net earnings of US$ 137 million in 2008, brought a negative return of US$ 68 million in 2009. Of course, both the demand and prices for diamonds are now showing an improved trend. The diamond business is therefore expected to present much better performance for 2010.

Be the first to comment